A CFO’s Guide to Smarter Healthcare Strategies

The right vendors make a difference—surround yourself with partners who prioritize fiduciary duty, transparency and flexibility, writes Roundstone’s Michael A. Schroeder.

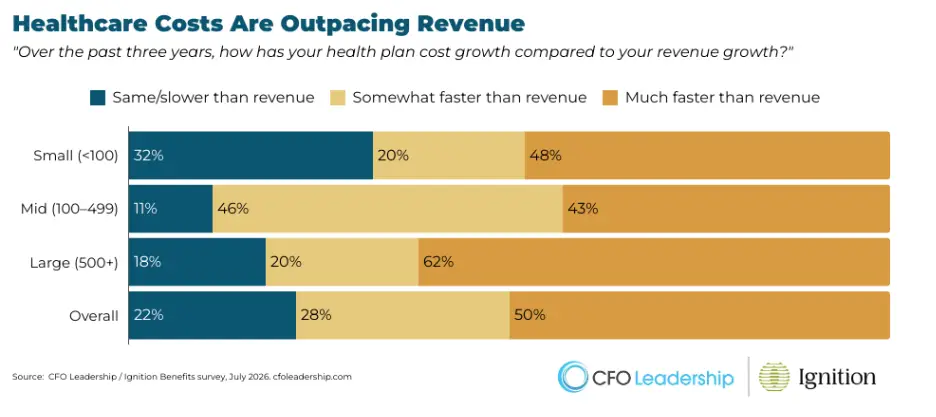

Potential Savings

There is another way. A quarter (28 percent) of the respondents to the Chief Executive Group/Roundstone survey indicated they had moved on from the traditional healthcare coverage benefit and invested in a self-funded healthcare plan with a stop-loss insurance policy that reimburses an employer for claims exceeding a specified threshold. Seven percent of respondents had invested in a self-funded plan that includes a captive solution with stop-loss coverage. But about half the respondents (47 percent) continued to be fully insured by a health insurance company.

After all, a traditional benefits plan from a health insurance company seems like a great deal from a risk management perspective. “A company that buys a fully insured program is paying the health insurer to take away its [financial] risk. If the insurer messes up and underestimates [employees’ annual claim costs], that’s on them,” says Andrew Coccia, senior manager of Deloitte’s human capital practice.

However, fully covered plans are not only constantly increasing in price year to year; they are also more expensive than self-funded alternatives.

For example, to mitigate the possibility of underestimating employee claims, the insurer tacks on a so-called risk charge. “If the insurer estimates the annual cost of claims for a company is about $10 million, they’ll add a 5 percent risk charge for moving the risk to their balance sheet, plus an additional amount to eke out a profit,” Coccia says. In addition, insurers typically add to the customer’s bill the one-to-three percent tax they pay on policyholder premiums,

An organization that self-insures liberates itself from the risk charge. However, the “profit charge” savings will probably be spent on purchasing stop-loss insurance to cover catastrophic losses.

Regardless, the expense savings of self-insuring are significant, resulting in positive net cash flow that can be allocated elsewhere. “We estimate that self-insured plans provide premium savings of 5 [percent] to 8 percent over the long run,” Coccia says.

Self-Funding Decisions

In general, size counts when weighing a move away from traditional full-coverage insurance. Large companies that make the transition often invest in a self-funded plan with a stop-loss insurance policy, plus or minus a captive insurance company. “If you’re in the Fortune 100 and you’re not self-insured, something weird is going on,” Coccia says.

After that, the decision to self-insure includes other factors. If an organization has roughly 500 employees in its health benefits program, Coccia explains, “the CFO has enough claims experience to be able to draw credible conclusions on future claims frequency to consider the benefits of self-insurance. The more employees, the more credible the conclusions and the more likely the employer is self-insured.”

Midsized and smaller companies with only a couple of hundred employees, however, would not automatically benefit from being self-insured. “They’d need to have a firm grasp of claims activity,” Coccia says.

Self-Insured Plus Stop-Loss

Self-insurance is not a cure-all. While the organization saves money, it has a higher administrative burden and risks exposure to catastrophic claims. To offset those disadvantages, employers typically engage a third-party administrator to assume the administrative work and, in conjunction, purchase stop-loss insurance.

That’s the strategy at CareCentrix, which purchases stop-loss insurance from Cigna. Cigna also manages the company’s self-insured healthcare plan.

“It would be hard for a single employer our size to administer the healthcare program,” says Phillip Shiver, CFO of the 1,700-employee provider of in-home care services. “You need a provider with a nationwide network to handle the claims processing, employee privacy issues, healthcare inquiries and other administrative tasks.”

CareCentrix has self-insured its employee healthcare plan since before Shiver joined the company in 2013. The self-insured plan and stop-loss insurance coverage have combined over the years to keep healthcare premiums flat.

In 2024, there was a “small bump” in the premium, reflecting higher healthcare costs, says Shiver. To moderate the impact, the company increased the point at which the Cigna stop-loss insurance policy kicked in—to $300,000 per occurrence, up from $250,000 previously. Nonetheless, the self-insured plan remains “significantly less expensive than buying a fully insured plan,” he says.

Like many employers that self-insure healthcare, CareCentrix invests in long-term strategies focused on reducing employee medical expenses, including wellness programs, preventive care and targeted interventions. “We offer cancer screening tests to catch potentially catastrophic conditions earlier, put together cooking seminars involving healthy eating and promote walking and other exercise events, where groups of employees participate in a variety of competitive races we call `Zombie Challenges,’” the CFO says.

Not surprisingly, given CareCentrix’s mission to “make the home the center of patient care,” its healthcare plan is structured to quickly redirect care to an employee’s home whenever medically feasible. “That’s a lot less expensive than a hospital setting and is also better for employees’ health and wellbeing,” Shiver says.

Self-Insured Plus Captive

The group captive that M. Davis & Sons joined as the twenty-sixth employer tallies several hundred like-minded organizations across various industries and sectors. “All the partners are striving for a cost-effective plan that’s in the best interests of employees,” says Gilmartin.

Gilmartin attributes the company’s average 4 percent increase in healthcare premiums over the past dozen years to the workshops, webinars and other gatherings where the captive’s members discuss their respective claims experiences and cost containment tactics. “We share our successes and failures,” he says.

An example involves employee emergency room visits, a key driver of healthcare plan costs. According to recent studies, a visit to the emergency room in the U.S. can cost $4,000 or more, depending on the severity of the medical condition. At a meeting with fellow captive members, Gilmartin learned that an unusually high number of ER visits were for relatively benign conditions, such as an earache—a medical issue addressable online, over the phone or at an inexpensive urgent care facility.

To discourage such visits in the future, the captive, Well Health Insurance, bumped up the price of going to an ER for such conditions.

Well Health was formed in 2011 by Captive Resources LLC, a consultant to member-owned group captives that encourages member companies to reimagine health insurance by taking control of it. This empowerment is evident in M. Davis & Sons’ decision to carve out coverage for expensive organ transplants from the captive’s medical stop-loss policy. A heart transplant, for example, typically costs more than $1 million, but only 3,700 are performed annually in the United States, according to Yale Medicine.

By removing the transplant coverage, M. Davis & Sons received a monthly $6,000 premium discount on its stop-loss policy. The surgeries are fully insured under separate insurance, priced at approximately $3,000 per month.

“We’ve had two kidney transplant cases with zero cost to the business or the individuals other than the annual premium for the carve-out coverage, demonstrating the carve-outs value as a targeted, cost-saving solution,” Gilmartin says.

A Choice For Small Companies

Smaller employers, such as Carta Healthcare, a provider of AI-fueled clinical data management solutions with 50 employees, also leverage the economies of scale offered by networking with like-minded employers. They do so through a professional employer organization (PEO). “We pool our healthcare coverages and expenses with hundreds of other small businesses in our PEO, Insperity, saving us 30 percent on average on our insurance costs,” says Carta Healthcare CFO Lucas Tanner.

PEOs function as the employer of record for multiple companies that employ between 25 and 250 employees, giving them greater clout to negotiate more favorable health insurance rates. “We analyzed what it would cost for comparable benefits from a fully funded health insurance plan and found that the savings from Insperity, our PEO, were significant, consistent with the other small companies I’ve served at as CFO,” Tanner says.

Down the line, Deloitte’s Coccia says that small, growing companies like Carta Healthcare are probably headed down a path toward a captive and self-insurance model. Given Carta’s May 2025 infusion of $18.5 million in Series B1 funding, such growth is in the cards.

“Like all forms of insurance, the greater the number of people insured, the greater the opportunity to spread the risk and seize economic value,” Coccia says. “That’s the law of large numbers.”